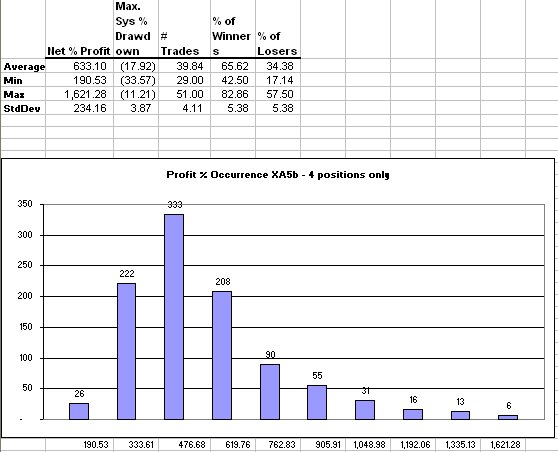

THis IO test shows an optimization on, of all things, buy and sell months. The buy month selected is May and the sell month is the following march. A 42 week ROC above 36 is a selection criteria, along with turnover. Exit trigger is either the month of March, or ROC below -23. Not suggesting that this is tradeable, it's just inspired by Dogs Of the Dow type strategies.

Posted by Picasa

Posted by Picasa