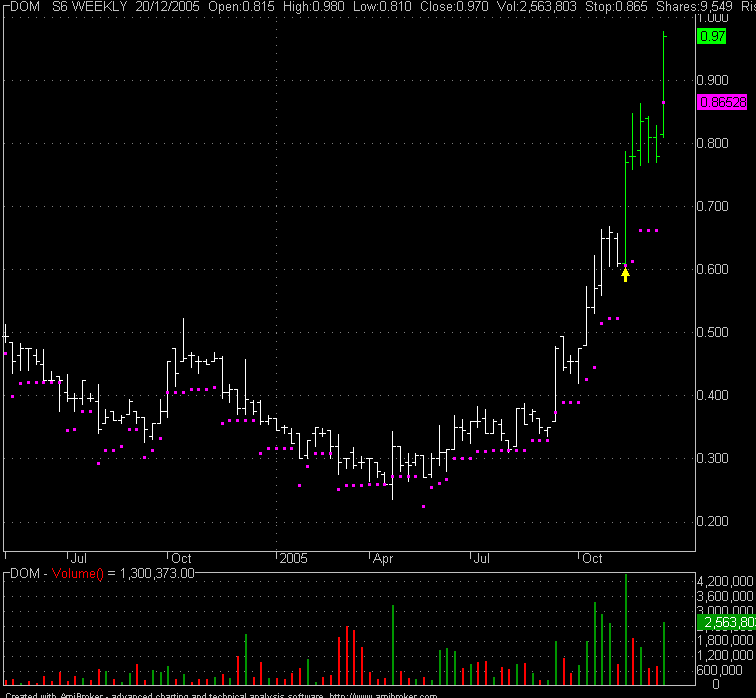

I prefer not to post trades in play in case someone thinks its a recommendation. I picked this one up with a system that doesn't give a lot of signals. Hopefully it pans out ok. It had already moved substantially before I jumped on, with signals firing much earlier in other systems.

Take the trade, follow the system, don't think too much and sell when I get the signal. The trailing stop should keep me out of too much trouble.